With the spotlight on artificial intelligence (AI) and megacap growth stocks, it’s easy to overlook the impressive run-up in stable stalwarts like Walmart (NYSE: WMT). Soaring just shy of 30% year to date, Walmart is the best-performing component of the Dow Jones Industrial Average — outpacing gains from Amazon, Microsoft, Apple, and other growth stocks. What’s more, Walmart has raised its dividend for over 50 consecutive years — making it a Dividend King.

Walmart has a clear plan for growing earnings and increasing its dividend — but the stock has gotten more expensive and the yield is just 1.2%.

Tool and outdoor products maker Stanley Black & Decker (NYSE: SWK) is also a Dividend King. But the stock is down over 10% in the last three months and a painful 57% over the last three years. Here’s why Stanley Black & Decker is out of favor, how it is turning things around, and why it is worth buying now.

A primer on Stanley Black & Decker

Stanley Black & Decker sells various hand tools, power tools, and accessories under brands like DeWalt, Stanley, Black+Decker, Craftsman, and others.

A whopping $13.4 billion or 85% of 2023 revenue came from its tools and outdoor segment, while just $2.4 billion came from its industrial business-to-business (B2B) segment. Sixty-two percent of 2023 sales were generated in the U.S. As such, the company has been heavily impacted by inflation, higher interest rates, weak consumer spending, and a challenged housing market. Meanwhile, other industrial companies that primarily engage in B2B sales — such as General Electric and Siemens — are hovering around all-time highs.

Peaks and valleys

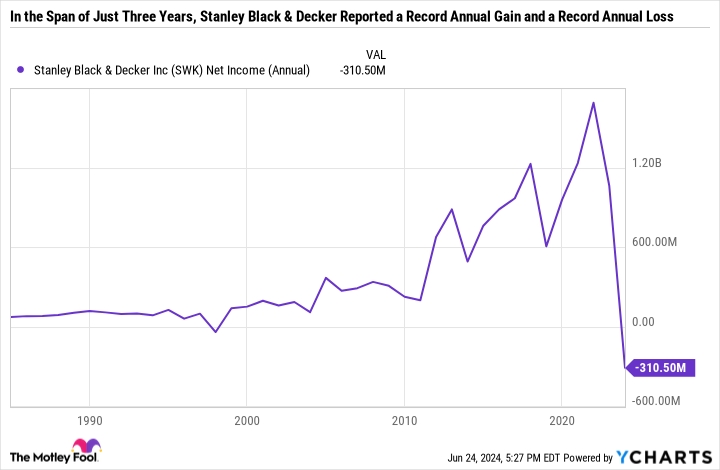

Stanley Black & Decker has been on a roller coaster over the last few years. It achieved all-time high net income of $1.69 billion in 2021, only to lose a record $311 million in 2023. The following chart paints this dramatic picture well.

You may be wondering how a company can go from a period of growth and expansion to a period of weakness in just a few years. The short answer is that the COVID-19 pandemic threw a wrench in the toolmaker’s business, disrupting supply chains and consumer behavior. Initially, Stanley Black & Decker benefited from a surge in goods spending, which is reflected in its 2021 results. But by 2022, it became clear that demand was merely pulled forward by a few years and that the boom was unsustainable.

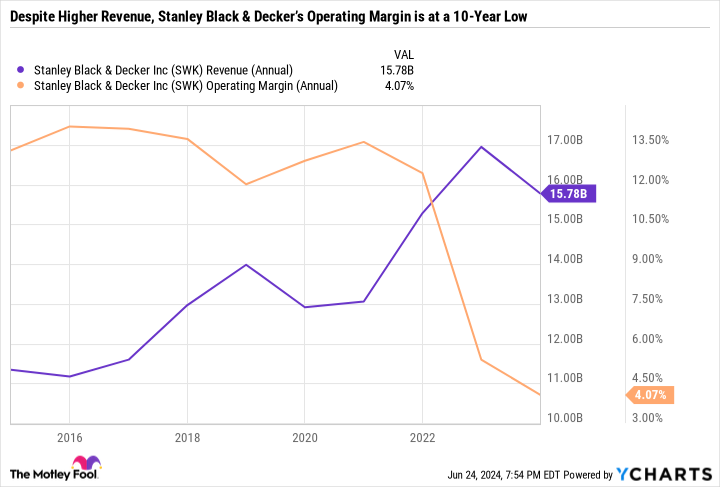

Stanley Black & Decker’s operating expenses increased to keep up with demand. But when demand fell, and revenue began to decline, those higher expenses ate away at margins. In 2023, Stanley Black & Decker had an operating margin barely over 4% compared to a pre-pandemic range of about 12% to 14% — illustrating how inefficient the business has become.

Getting back on track

The company has implemented a massive cost-cutting effort to restore margins — with a goal of reaching an adjusted gross margin of 35% over the long term and 30% for full-year 2024. Stanley Black & Decker achieved $145 million in pre-tax cost savings last quarter, bringing its aggregate cost savings to $1.2 billion since the program was launched in the second quarter of 2022.

To its credit, Stanley Black & Decker has stayed on track toward hitting its goals. When it first announced the program, it was guiding for $1 billion in pre-tax savings by the end of 2023 and $2 billion in savings within three years. During its first-quarter 2024 earnings call, Stanley Black & Decker said it was still targeting $1.5 billion in pre-tax run-rate savings by the end of 2024 and $2 billion by the end of 2025.

Reducing inventory has been another focus for the company. Stanley Black & Decker is forecasting $400 million to $500 million in inventory reductions for the full year and capital expenditures of just $400 million to $500 million. Reducing inventory and keeping a tight lid on spending should help the company reach its free-cash-flow (FCF) goal of $600 million to $800 million for the full year. That’s still a way off from the $1.08 billion in FCF the company earned in full year 2019, which is a good benchmark considering it’s before the pandemic disrupted its business.

A high yield with a (potentially) inexpensive valuation

2024 FCF guidance would allow Stanley Black & Decker to cover its dividend with FCF. In the recent quarter, Stanley Black & Decker paid $121.8 billion in dividends. Over the last couple of years, it has made minimum $0.01-per-share-per-quarter dividend raises to retain its status as a Dividend King — which is understandable given the business is undergoing a turnaround. Therefore, investors should expect minimum raises over the next few years as well, meaning the annual dividend expense should be under $500 billion for 2024 and 2025.

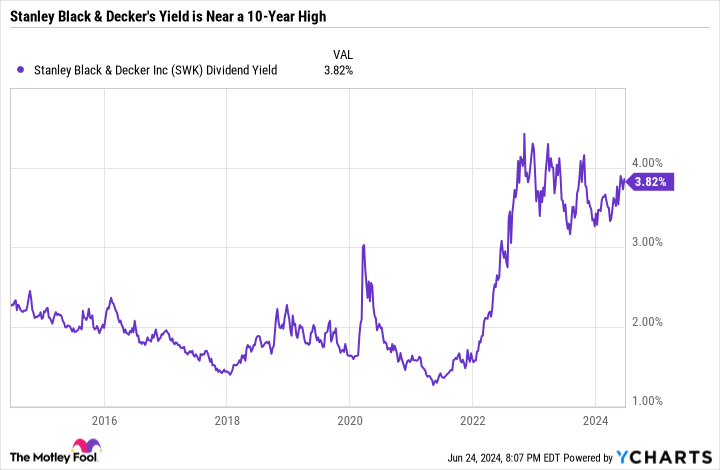

A lower stock price paired with a moderately higher dividend has pole-vaulted Stanley Black & Decker’s yield to 3.8% — which is significantly higher than the 2% or so yield investors were getting pre-pandemic.

Given its net loss in 2023, Stanley Black & Decker currently has a negative price-to-earnings (P/E) ratio. However, analyst estimates reflect the impact of its cost-cutting efforts and a return to profitability. Average analyst estimates call for $4 in 2024 earnings per share (EPS) and $5.48 in 2025 EPS. Based on the 2025 EPS guidance, Stanley Black & Decker would have a P/E ratio of just 15.5 — which is dirt cheap for a Dividend King. However, a lot could go wrong between now and when that full-year 2025 figure rolls in — so investors shouldn’t bank on analyst estimates.

Stanley Black & Decker is worth the wait

Stanley Black & Decker poorly navigated the COVID-19 pandemic, supply chain disruptions, and interest rates. And the stock price reflects these mistakes — as it is just 15% or so off its 10-year low. However, the company has been doing a good job over the last seven quarters by sticking to its cost-cutting plan.

In the near term, Stanley Black & Decker’s FCF projections indicate confidence that it can support its dividend with cash. Over the medium term, a return to profitability and earnings growth makes the stock look like a good value.

Even as the business recovers, investors shouldn’t expect the company to drastically increase its dividend or buy back stock. The balance sheet has weakened in recent years due to higher debt. S&P Global‘s June 20 annual review of the company gave it an A- credit rating, which is good but could be improved.

At times like this, it’s important to zoom out and think about where a business will be three to five years from now. If Stanley Black & Decker can return to its pre-pandemic form and chart a path toward growth, the valuation and yield will make the stock look too cheap to ignore. Patient investors may want to scoop up shares of the Dividend King now, while others may prefer to take a wait-and-see approach to ensure Stanley Black & Decker can effectively operate under a leaner business model.

Should you invest $1,000 in Stanley Black & Decker right now?

Before you buy stock in Stanley Black & Decker, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Stanley Black & Decker wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $759,759!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of June 24, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Apple, Microsoft, S&P Global, and Walmart. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Walmart Is a Rock-Solid Dividend King, but So Is This High-Yield Dividend Stock That’s Down 11% in the Past 3 Months was originally published by The Motley Fool

Source link